It reminded me of a speech that the prime minister gave last spring to the German-Hungarian Chamber of Industry and Commerce. In the prime minister’s characteristic ‘straight talk,’ he laid out in frank terms the difference in views in Europe on fiscal deficits and debt. “There are a great many people,” he said,

“who envisage the future of Europe by drawing on the Germans’ money, one way or another, to get out of the macro-economic trouble they are in. To justify this, some inventive solutions have been conceived with the aid of spectacular linguistic artifice – “communal effort”, and some other expressions that are hard to construe – the essence of which may be summed up in every instance as drawing on the Germans’ money as part of our joint responsibility.”

Hungarians, he said, see it differently.

“[W]e are indeed an adherent of that policy [of fiscal discipline] (because we believe Chancellor Merkel, who says that sooner or later we must work for every penny we spend), but it also means that we do not like to live off other people’s money, because sooner or later this will lead to the loss of our dignity, the evaporation of respect for our nation and a degree of subordination; this is something that the Hungarians do not tolerate well.”

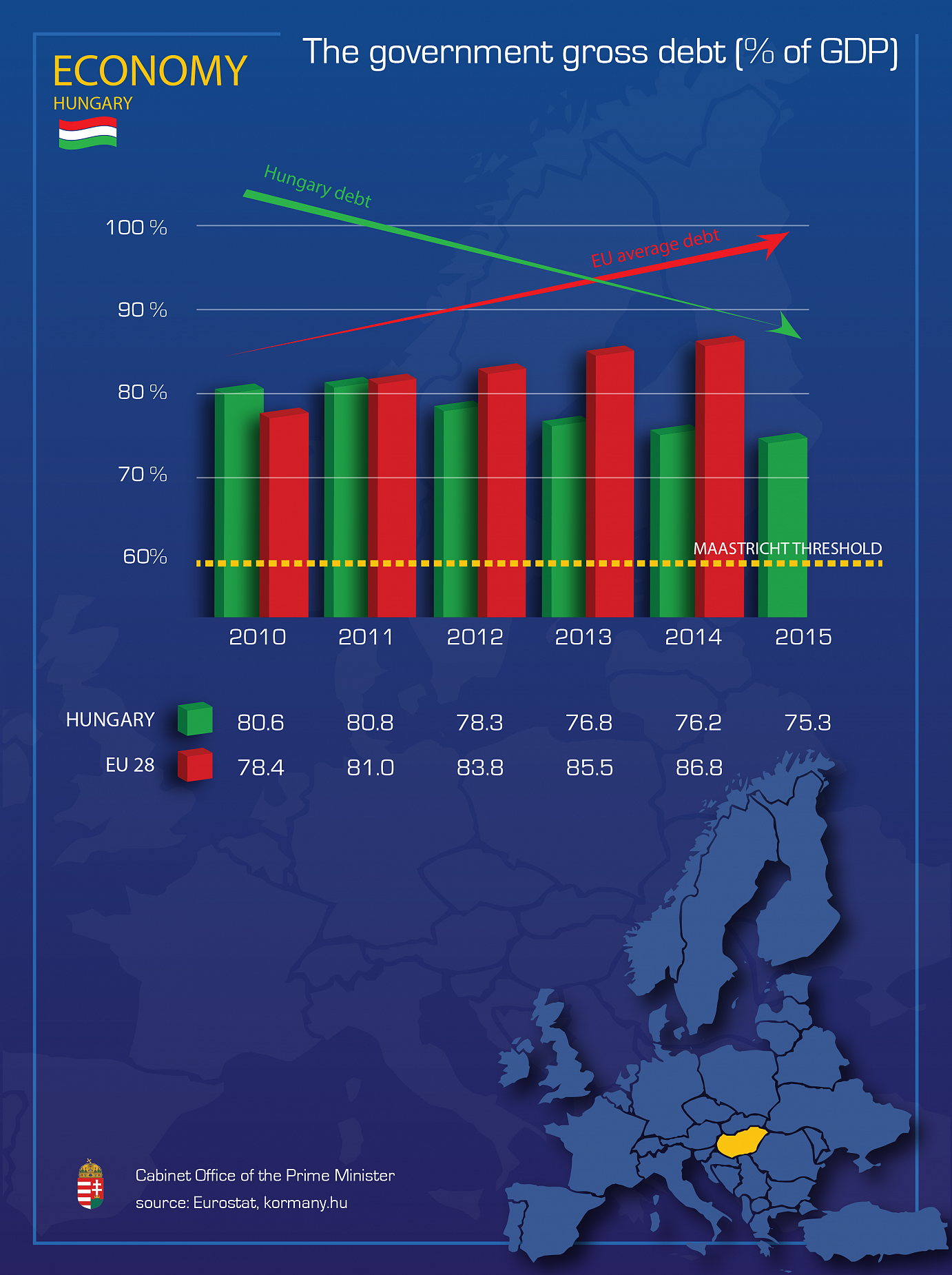

That’s the vision that has guided the Orbán Government since taking office in 2010 and the reason we are paying off our loans, reducing our debt and cutting the deficit.

This week, Hungary made the last payment of 1.5 billion EUR to the European Commission, paying in full a loan taken by the previous Hungarian government. With this last payment, said Minister for National Economy Mihály Varga at a press conference on Wednesday, the Orbán Government has taken yet another step toward our goal of economic stability and financial independence.

The 2008 financial crisis hit Hungary’s economy hard and, as this article on About Hungary explains, the crisis exploited a number of structural problems, such as the rising external debt. These structural weaknesses were aggravated by the failed economic policies of previous left-wing governments, policies that forced austerity measures, tax increases and other burdens on families. By the end of 2008, Hungary was near bankruptcy, and the Socialist government was forced to request a loan from the IMF, the EU and the World Bank.

By 2010, Hungary’s debt-to-GDP ratio soared dramatically from 55.1 percent in 2002 -- that’s when the first Orbán Government left office -- to 83.7 percent under the Socialists. Spending pushed the deficit up to 7 percent of GDP.

As Minister Varga pointed out during his press conference last week, the structure of state debt had also become a serious risk in a volatile international financial market: 70 percent of Hungary’s debt was financed by foreign creditors, and the share of forex debt had hit 50 percent of the total debt.

Beginning in 2010, however, the health of the state budget began to improve, and in 2013, the economy began to grow again, resulting in the suspension of the EU’s excessive deficit procedure against Hungary.

By the summer of 2013, Hungary repaid the IMF loan of 8.8 billion EUR ahead of schedule. The transfer of 1.5 billion EUR on Wednesday was the last tranche of the 5.5 billion EUR loan from the European Commission, finally settling the debt.

Today, 89 percent of Hungarian debt is in state bonds, Minister Varga said, while the rate of debt in foreign currency and of foreign creditors has dropped considerably.

Hungary has not always been so fortunate, however. As the prime minister said in the State of the Nation address earlier this year, “While the other [countries] were rising, we found ourselves mired in growing sovereign debt, crippling foreign currency mortgage loans, high budget deficits, rampant inflation, a balance of payments deficit and rising unemployment. This was eventually followed by financial ruin, a dog-collar and leash held by the IMF, and debt slavery.”

But within three years, the Orbán Government, “consolidated the budget, stabilised the economy, avoided bankruptcy, curbed inflation and reduced unemployment – the latter not marginally, but from 11.5 percent to 6.2 percent. We sent the IMF packing, repaid our loan ahead of schedule, and this year we shall also repay the last blessed penny of our debt to the European Union.”